How to Get Out of a Car Finance Agreement: Your Guide to Voluntary Termination

Life changes, and your car finance agreement doesn't always change with it. Whether your circumstances have shifted or the monthly payments no longer work for you, the good news is that UK law gives you more options than most motorists realise.

Whatever your situation, there’s no need to panic. Voluntary termination is an option you can take to end your car finance agreement.

This guide explains exactly what voluntary termination is, how it works, when you can use it, and what it means for your credit file. By the end, you will know your rights and how to use them confidently.

What Is Voluntary Termination on Car Finance?

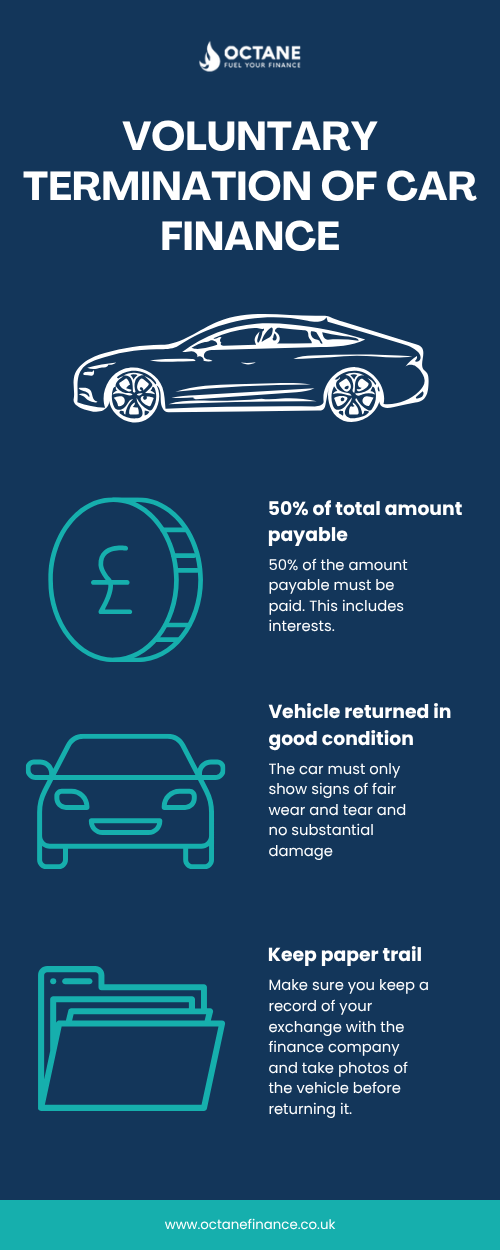

Voluntary termination (VT) is a legal right that allows you to end a car finance agreement early by returning the vehicle to the lender, provided you have met specific conditions. This is a statutory right that you can find in Section 99 of the Consumer Credit Act 1974.

The act states that: if you have paid at least 50% of the total amount payable under your agreement, you can hand the car back, provided the vehicle is returned in good condition, and there are no outstanding payments.

This right applies to two of the most common types of car finance in the UK: Hire Purchase (HP) and Personal Contract Purchase (PCP).

Car Finance Termination Rights: What the Law Actually Says

Section 99 of the Consumer Credit Act 1974 exists to protect consumers who take out regulated credit agreements. It gives borrowers the right to terminate an HP or PCP agreement at any point, providing:

- At least 50% of the total amount payable has been paid (or you make up the difference at the point of termination)

- The vehicle is returned in a condition consistent with fair wear and tear

This is an important distinction from voluntary surrender, where a borrower hands the car back before reaching the 50% threshold. Voluntary surrender can result in a shortfall that the lender may pursue, and it is more likely to negatively impact your credit file. Voluntary termination under Section 99, by contrast, is a clean legal exit.

Voluntary Termination HP vs PCP: Is There a Difference?

Voluntary Termination HP

With Hire Purchase, calculating your 50% threshold is straightforward. It is half of the total amount payable, which includes the deposit, all monthly instalments, and any fees stated in the agreement. Once you have paid this amount, you can exercise your right to terminate.

PCP Early Termination

PCPs work slightly differently because there is a balloon payment at the end. The key point here is that the optional final balloon payment is included in the 50% calculation. This means voluntary termination on a PCP is often triggered after the midway point of the contract.

If you are not yet at the 50% mark, you will need to make up the shortfall before you can complete the termination.

How to Get Out of a Car Finance Agreement: Step by Step

If you have decided that voluntary termination is the right route, here is how the process works in practice.

Step 1: Check your agreement

Pull out your finance agreement and find the total amount payable. Now you just need to calculate 50% of that figure. The last thing to do is to check your payment history to see how much you have already paid, including your deposit and all monthly instalments.

Step 2: Contact your lender in writing

Having a paper-trail is better than a phone call, so make sure you put things in writing. Send a voluntary termination car finance letter to your lender that clearly states you are exercising your right under Section 99 of the Consumer Credit Act 1974. There are a few things you should include in your letter, and we’ve put together a template so you don’t have to guess what is needed.

Voluntary Termination Car Finance Letter Template

- Your full name and address

- Your finance agreement reference number

- Your vehicle details

- A clear statement that you are exercising your right to voluntary termination under Section 99 of the Consumer Credit Act 1974

- The date you wish to return the vehicle

- A request for written confirmation from the lender

Make sure you keep a copy of everything you send, so you can always refer back to your communication whenever you need.

Step 3: Pay any shortfall

If you have not yet reached the 50% threshold, you will need to pay the difference before or at the point of return. Your lender should confirm the exact figure.

Step 4: Return the vehicle

Arrange to return the car to the lender or their nominated location. The vehicle must meet the fair wear and tear standard (more on this below). Make sure you document the car's condition with photographs before handing it over.

Step 5: Get written confirmation

Once the car has been returned and any outstanding payments settled, request written confirmation from the lender that the agreement has been terminated. This protects you if any queries arise later.

Voluntary Termination of Car Finance and Fair Wear and Tear

One of the most misunderstood parts of the voluntary termination process is the condition the car must be returned in. Lenders will inspect the vehicle, and any damage beyond fair wear and tear may result in additional charges. You might be wondering what is considered fair wear and tear.

Fair wear and tear refers to the normal deterioration expected from everyday use over the length of the agreement. It does not mean the car needs to be showroom-perfect, but it does mean you are responsible for any damage beyond what would be reasonably expected.

Examples of fair wear and tear typically include minor surface marks, small stone chips, and light scuffs consistent with normal driving. Examples of damage that may attract charges include large dents, deep scratches, damaged interior trim, missing parts, and worn tyres below the legal limit.

The British Vehicle Rental and Leasing Association (BVRLA) publishes a fair wear and tear guide that many lenders use as their benchmark. Checking this before you return the vehicle will give you clear expectations and reduce the likelihood of disputes.

We said this before, but we’ll say it again because it’s really important: before handing the car back, take photographs of every panel, the interior, wheels, and any existing marks. This documentation protects you if the lender later claims damage that was already present.

Does Voluntary Termination of Car Finance Affect Your Credit Rating?

This is one of the most common concerns for anyone considering voluntary termination, and it’s a fair question.

Voluntary termination does not, in itself, damage your credit score. It is a legal right, and exercising it is not the same as defaulting on a loan or missing payments. The termination will, however, appear on your credit file. As long as you have met all your financial obligations under the agreement and paid any balance owed to reach the 50% threshold, your credit score should not be negatively affected by the termination.

If you are in any doubt about how a VT might be recorded on your credit file, you can check your credit report with a credit reference agency. Free options include ClearScore (powered by Equifax data) and Credit Karma (powered by TransUnion data). Experian also offers a free statutory report.

Other Ways to Get Out of a Car Finance Agreement

Voluntary termination under Section 99 is not your only option for ending car finance early. Here are the other main routes:

Settle the finance early. You can request a settlement figure from your lender at any time. This is the amount needed to pay off the agreement in full. Early settlement may come with a small interest charge (typically one to two months' interest), but it gives you immediate ownership of the car and a clean end to the agreement.

Part-exchange or sell the car. If there is equity in the vehicle (meaning it is worth more than the outstanding balance on the finance), you can sell it and use the proceeds to settle the remaining balance. Any surplus goes to you. If the car is worth less than the outstanding balance on the finance, you will need to make up the difference.

When Voluntary Termination Makes Sense

If you're unsure whether VT is the right choice, there are some situations where it is an option worth considering.

- Your financial circumstances have changed materially since you took out the agreement

- You no longer need the vehicle, for example, due to a change in work or lifestyle

- You are approaching the end of the agreement and would prefer not to make the balloon payment on a PCP

If you find that the monthly payments have become unaffordable, we advise you to seek impartial advice. Free support and advice are available from MoneyHelper or StepChange.

Getting the Right Advice Before You Act

If you are unsure whether voluntary termination is the right move for your situation, it is always worth speaking to a specialist before making any formal request to your lender.

At Octane Finance, we work with a wide network of lenders across all types of vehicle finance, including car, motorbike, prestige, and classic vehicle agreements. Whether you are looking to exit your current arrangement, explore refinancing options, or find a new deal that better fits your circumstances, our team, with over 2,000 five-star Trustpilot reviews, is here to help.

Get in touch today to talk through your options, no obligation, no mark on your credit file at the initial enquiry stage, and straightforward advice from people who understand the vehicle finance market inside out. Subject to status and affordability.

Voluntary Termination FAQs

Can you return a financed car whenever you like?

Not without financial consequence. If you want to return the car before reaching the 50% payment threshold under a VT, you would be doing so under voluntary surrender rather than voluntary termination. This means the lender can pursue you for any outstanding balance. To exercise your legal right under Section 99 of the Consumer Credit Act 1974, you must have paid at least 50% of the total amount payable.

Does voluntary termination of car finance affect your credit rating?

Exercising your right to voluntary termination should not damage your credit score, provided you have met all financial obligations, including any shortfall payments and charges for damage. The termination will appear on your credit file, which some lenders may consider when evaluating future applications, but it is not treated the same as a default or a missed payment.

How do I write a voluntary termination letter for car finance?

Your letter should clearly state that you are exercising your right to voluntary termination under Section 99 of the Consumer Credit Act 1974. Include your full name, address, finance agreement reference number, and a request for written confirmation. Send it by email or recorded post so you have proof of delivery. Keep a copy for your own records.

Does voluntary termination apply to personal loans?

No. Voluntary termination under Section 99 only applies to regulated HP and PCP agreements. Personal loans are unsecured and not covered by this legislation.

How long does voluntary termination take?

The process typically takes a few days to a few weeks, depending on the lender. Once your written notice has been received and acknowledged, the lender will arrange the collection or return of the vehicle and conduct its inspection. Any shortfall payments or damage charges must be settled before the agreement is formally closed. Keep all correspondence until you receive written confirmation that the agreement has ended.